![]()

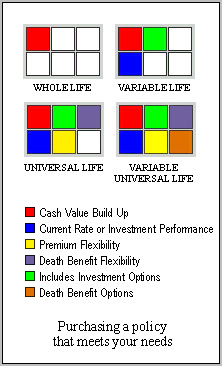

Forward The Universal Life landscape has not changed all that much since its inception. It's main components premium flexibility, competitive returns and guaranteed coverage keep this product at the forefront of the insurance industry. The HistoryUniversal Life (UL) can best be described as an interest sensitive life insurance program developed as a result of disintermediation challenges that faced the life insurance industry in the late 70's early 80's. Prior to the introduction of UL policies, whole life and term insurance were really the only two games in town. However, when interest rates skyrocketed and mutual funds and money markets became the preferred choice of investing, whole life insurance (which was supported by suffering long term bonds and mortgage portfolios at the time) looked like a poor place to keep your money. Money Out, Money InAs a result, dollars fled from whole life policies and the industry was forced to change in order to stay competitive. UL was born and now offered money market-type rates within the insurance company policy. This put the industry back into a competitive position for the consumer's dollar. Hence, within a relatively short period of time, UL became an attractive concept for those preferring current competitive rates of return (with life insurance protection) versus long term bond or mortgage type yields seen in whole life policies.

|

Copyright 1998

Fielder Financial Management, LTD.

All Rights Reserved.

Securities offered through Fortune Financial Services, LLC. member FINRA, SIPC. Fielder Financial Management, Ltd. not affiliated with Fortune Financial Services, LLC. Mark Fielder, Financial Professional, CA. Insurance Lic. # 0690576.

Today

Today