![]()

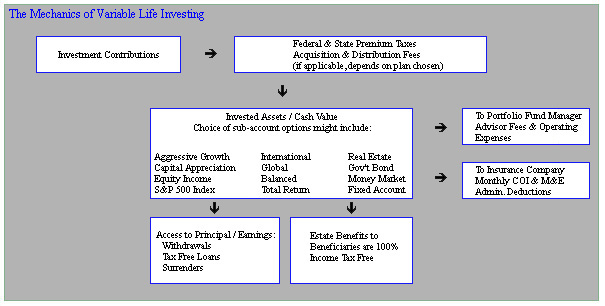

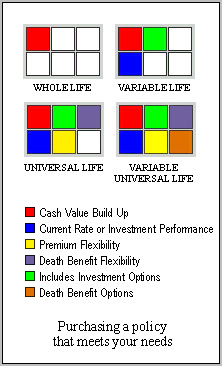

Forward Variable Life is one of the most popular forms of insurance investing today. It has been commonly referred to as the "Swiss Army Knife" of the insurance business because of its many features and uses. When properly set up and maintained, it offers extraordinary flexibility and significant tax advantages. Today, investors will use Variable Life plans as a supplemental retirement income vehicle. History Much has been written about the wide variety of uses that Variable Universal Life (VUL) Insurance offers especially over the decade as it's popularity has increased. You may have heard VUL plans called or referred to as various surnames including 'private pension plan', 'private retirement option', 'insurance-based retirement plan', or '5x7 Pay Life'. VUL was first introduced in the U.S. marketplace by Equitable Life in the mid 1970's. It was fairly slow to develop primarily due to three reasons; 1) the question of how the product was to be governed given it's 'variable' nature; 2) selling agents/brokers were required to hold a FINRA (NASD) securities license; and 3) the longer-than-anticipated educational curve needed in the consumer marketplace. The Securities & Exchange Commission and state insurance commissioners finally agreed how it was to be registered and regulated in 1976 and enacted rule 6E-2. This rule provided the guidelines on how these policies were defined under the Investment Company Act of 1940. And it is for these reasons that VUL plans are offered by a prospectus only. The first generation of VUL products was (by today's standards) rather expensive products. As time passed, product features were enhanced and the chassis became more and more streamlined as investors demanded lower cost plans. As a result, Variable Life purchases have grown steadily the past 20 years. Why the Attraction? Although very much similar to a whole life or a universal life policy in that you have a stated current and guaranteed death benefit, premium pay in options and cash values, the major difference lies in the control issue and potential earnings power. Of course, the death benefit is based on the claims-paying ability of the issuer. In a traditional whole life or universal life policy, the customer was (and still is) at the mercy of the insurance company to credit a respectable yield or annual dividend. Under a VUL contract, the policyholder has complete discretion on how to allocate his or her premiums among the various investment sub-accounts available within the product they own. For example, many of the more progressive VUL sponsors will allow their policy holders to pick and choose from 20 or more investment sub-account options which are managed by professional fund groups such as Fidelity, Janus, American Century, Oppenheimer, Nationwide, Blackrock, Franklin-Templeton, Putnam and other well-known money management groups. Typical VUL sub-accounts Offered:

Further, the policyholders are typically not restricted from moving in and out of these various sub-accounts based on their personal choices - free of loads, commissions and capital gains.

|

Copyright 1998

Fielder Financial Management, LTD.

All Rights Reserved.

Securities offered through Fortune Financial Services, LLC. member FINRA, SIPC. Fielder Financial Management, Ltd. not affiliated with Fortune Financial Services, LLC. Mark Fielder, Financial Professional, CA. Insurance Lic. # 0690576.

Disclosure: For more complete information about variable life, including charges and expenses, obtain a prospectus by calling 1-800-480-7526. Read it carefully before you invest or send money. Investment return and principal value of an investment will fluctuate. An investors units, when redeemed, may be worth more or less than their original investment. Consult your tax advisor. Above, the information mentioned two (2) other types of insurance policies: traditional whole life and universal life. In the context of this information, these two (2) types of policies are of the fixed yield or fixed annual return nature. These types of insurance contracts are not offered by a prospectus and are not governed by the NASD or SEC. However, so the reader of this page better understands, in these types of policies the COI's, mortality & expense fees, the administrative costs, the distribution costs, any applicable flat extras or table rating, commissions, et. al. are 'bundled' and generally not explicitly definable. In contrast, a VUL policy is an 'unbundled' insurance plan for which any consumer may clearly define what these types of expenses associated with the product are. AS NOTED ABOVE, please read the prospectus. It will contain all charges, expenses and risks.

*As reported by the National Underwriter, Sept. 2000

Income & Estate Tax Advantages

Income & Estate Tax Advantages